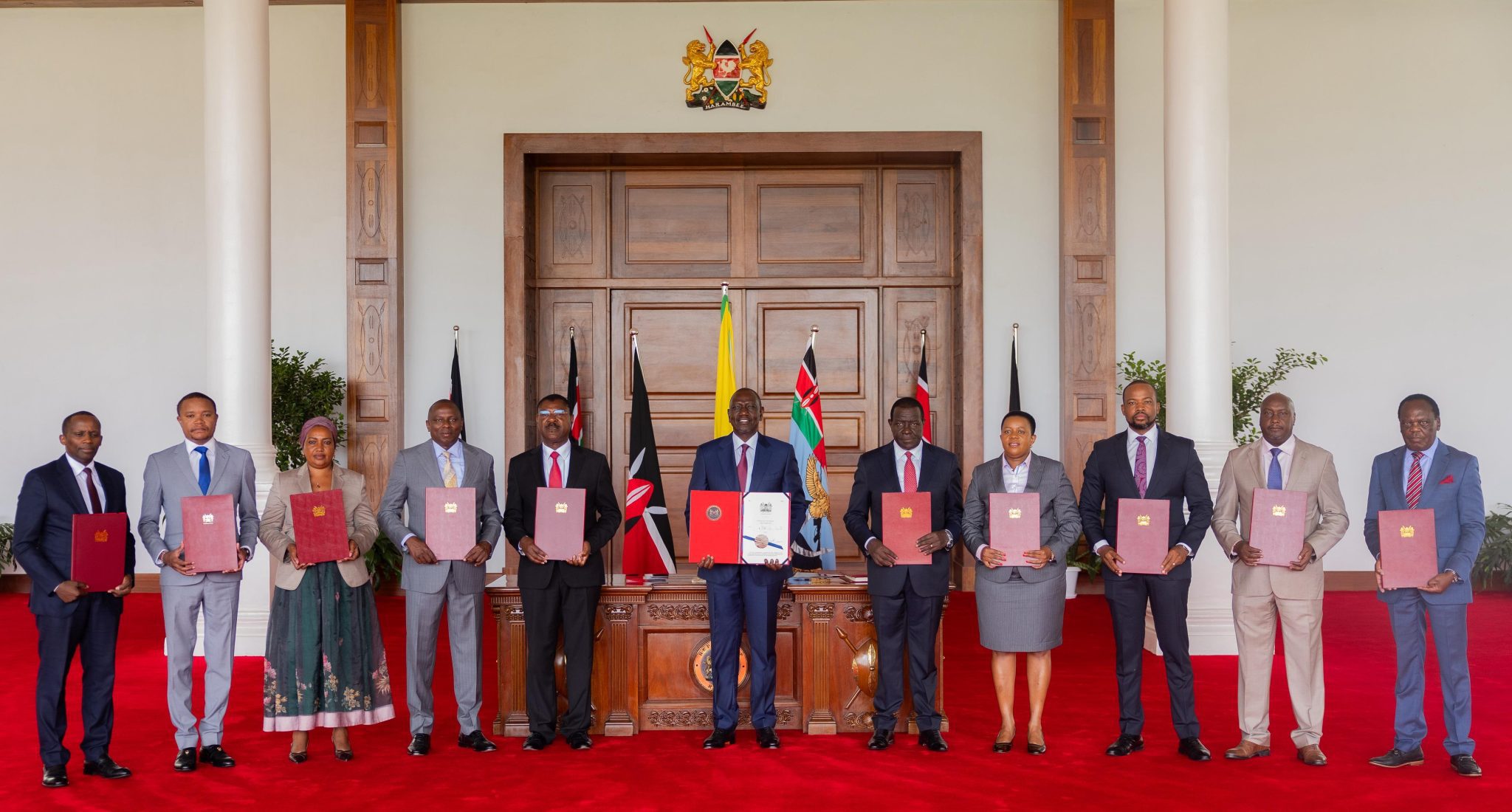

In a significant policy move with far-reaching economic and security implications, President William Ruto signed into law the Anti-Money Laundering and Combating of Terrorism Financing Laws (Amendment) Bill, 2025. The legislation, which revises ten existing Acts, is expected to fortify Kenya’s financial regulatory framework and unlock as much as KSh 100 billion in investment confidence and economic safeguards.

The new law introduces critical protections to prevent the misuse of Kenya’s financial and property sectors for money laundering and terrorism financing. Its enactment comes at a pivotal time as the country works to resolve outstanding technical deficiencies flagged by the Financial Action Task Force (FATF) and the Eastern and Southern Africa Anti-Money Laundering Group (ESAAMLG).

The amendments target structural weaknesses across various sectors that have historically been exploited to hide illicit funds, including real estate, mining, gaming, pensions, cooperative societies, and professional services. This multifaceted reform effort not only enhances Kenya’s legal defenses against transnational financial crime but also lays the groundwork for Kenya’s removal from the FATF grey list—a designation that has, until now, impeded global investor confidence and cross-border financial partnerships.

By closing long-standing loopholes, particularly in property transactions and shell companies, Kenya is reinforcing its credibility as a safe and transparent investment destination. For a country that remains a major economic hub in East Africa, the strategic importance of insulating its financial system from criminal exploitation cannot be overstated. Illicit financial flows have often been linked to regional terrorism networks, making this legislative step as much a security imperative as it is an economic one.

The sweeping reform amends ten Acts of Parliament, including the Proceeds of Crime and Anti-Money Laundering Act, the Prevention of Terrorism Act, and laws governing sectors such as betting, mining, retirement benefits, SACCOs, and professional services. Collectively, these changes align Kenya with international anti-money laundering and counter-terrorism financing standards.

The government anticipates that the reforms will inject regulatory clarity into sectors critical to economic growth. With stronger oversight in high-risk sectors like mining and real estate, Kenya is poised to attract new waves of foreign direct investment. This clarity also supports the formalisation of previously under-regulated economic activities, thus broadening the national tax base and contributing to long-term fiscal sustainability.

Simultaneously, President Ruto assented to the Insurance Professionals Bill, which lays out a robust legal framework to regulate the insurance industry. This law establishes key institutions such as the Insurance Institute of Kenya and the Insurance Professionals Examinations Board, tasked with enforcing high standards, professional discipline, and continuous development within the sector. It is expected to raise consumer confidence and professional accountability in a sector vital to financial stability and personal risk protection.

Together, these legal frameworks reflect Kenya’s strategic pivot towards transparency, security, and economic resilience. They strengthen the country’s position as a regional financial hub while also shielding it from the destabilising effects of financial crime and terrorism.

With the full weight of the presidency and Parliament behind these measures, Kenya is sending a clear message to global partners, investors, and regulators: the country is committed to high standards of integrity and accountability. This is more than legislative housekeeping; it is a transformational step toward secure, inclusive, and sustainable economic growth.

Kenya has secured a Sh22 billion financing package from Japan, marking a major milestone in the country’s industrialization agenda and strengthening bilateral economic cooperation. The funding, signed between...

Read moreDetails

{kind=link}