Kenya is edging closer to a historic economic milestone after the government confirmed that the first commercial crude oil export from Turkana is scheduled before the end of 2026. Speaking during a televised interview on February 24, 2026, Energy Cabinet Secretary Opiyo Wandayi said the country expects the first batch of oil drilled in Turkana to be transported to the Port of Mombasa for export by December. The announcement signals Kenya’s long-awaited entry into the league of oil-producing nations.

Initial production under the South Lokichar development plan is projected at 20,000 barrels per day, with output expected to scale up to 50,000 barrels per day as infrastructure and field development advance. The ramp-up reflects growing investor confidence and steady progress in unlocking the commercial potential of the Turkana oil fields, which have remained largely untapped for years.

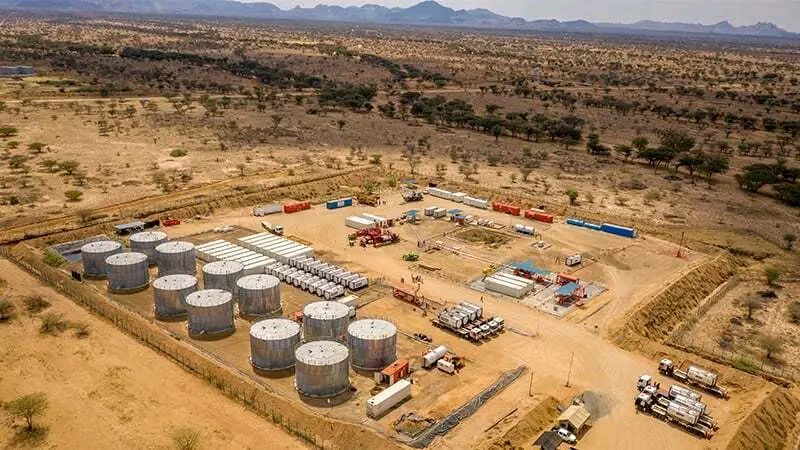

The breakthrough follows parliamentary deliberations on the Field Development Plan (FDP), a critical step in paving the way for full-scale production. Appearing before a Joint Parliamentary Committee on Energy, Francis Njogu, Chairman of Gulf Energy E&P BV, described the South Lokichar Oil Project as Kenya’s most significant privately funded upstream petroleum venture. Lawmakers overseeing the review include National Assembly Energy Committee Chairman David Gikaria and Senate Energy Committee Vice Chair William Kisang.

Gulf Energy E&P BV has committed approximately Ksh774 billion to the project, underscoring the scale of capital required to bring Turkana’s oil reserves to market. The firm has secured financial backing and credit lines from leading local and international banks, ensuring that funding constraints do not derail progress. Njogu announced December 1, 2026, as the formal production target date, pending expedited ratification of the FDP.

The economic implications are profound. Government projections estimate lifetime earnings ranging from USD 1.05 billion at an oil price of USD 60 per barrel to USD 2.9 billion at USD 70 per barrel—equivalent to roughly Ksh136 billion to Ksh371 billion. These revenues could significantly boost Kenya’s fiscal position, expand public investment capacity, and ease pressure on debt servicing obligations.

Beyond direct revenues, oil exports are expected to strengthen Kenya’s foreign exchange reserves and support the stability of the shilling. By reducing reliance on imported petroleum products, the country stands to cut its import bill substantially. This shift would help narrow the trade deficit and shield the economy from global oil price shocks that often strain foreign currency reserves.

The project is also poised to create thousands of jobs across the value chain—from drilling and logistics to transport, engineering, and support services. Gulf Energy has pledged to prioritize local employment, especially within the Turkana host community, fostering inclusive growth. As production scales toward 50,000 barrels per day, ancillary sectors such as construction, hospitality, and supply chain services are expected to benefit.

In the long term, full-scale development of the Turkana oil fields could reduce energy costs for manufacturing industries, enhancing Kenya’s competitiveness as a regional industrial hub. Affordable and locally sourced energy would lower operational expenses, stimulate industrial expansion, and attract foreign direct investment. If executed effectively, the South Lokichar project could mark a transformative chapter—positioning Kenya not only as an oil exporter but as a stronger, more self-reliant economy.

{kind=link}