Kenya’s economic stability is gaining renewed momentum as multiple macroeconomic indicators point to a stronger and more resilient outlook heading into 2026. A new World Bank assessment highlights significant progress across credit markets, external balances, inflation management, and sectoral performance—offering much-needed optimism after a challenging period marked by fiscal pressures and global uncertainty.

One of the strongest signals of renewed stability is the sharp improvement in private sector credit. After contracting by 2.9% in February 2025, credit growth rebounded to about 5% by August 2025. This shift underscores improving monetary policy transmission and recovering confidence among lenders, enabling businesses to access financing needed for expansion, investment, and job creation.

Business conditions have also strengthened, with the Purchasing Managers’ Index (PMI) recovering to above 50 in October 2025 after four months of contraction. This marks a return to growth in output, sales, and employment across surveyed firms, reflecting improved domestic demand and operational stability within the private sector.

Inflation continues to trend downward despite temporary volatility in items such as housing, utilities, and transport. Headline inflation eased from 6.9% in October 2023 to 4.7% in October 2025. Core inflation components remain stable, suggesting underlying price pressures are moderating and providing consumers with relief as economic activity normalizes.

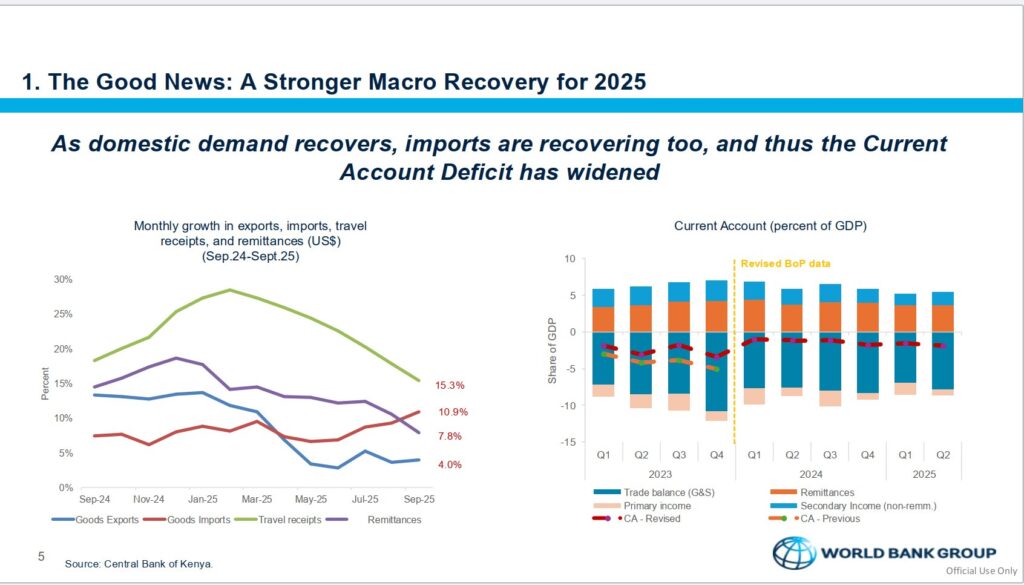

On the external front, Kenya’s foreign exchange reserves have surged from about $7.1 billion to $12.2 billion—a level equivalent to roughly 5.5 months of import cover. This historically strong buffer significantly reduces external vulnerability and boosts investor confidence at a time when global markets remain uncertain. The improvement is supported by a balanced external sector: as of September 2025, imports grew by 10.9%, exports by 4%, and travel receipts remained robust at 15.3%, underscoring vibrant tourism activity and resilient export performance.

Remittances, a key pillar of household income and foreign exchange inflows, rose 7% year-on-year by September 2025. This steady growth continues to anchor family welfare and support domestic consumption, especially in rural and peri-urban areas.

The current account deficit widened slightly to 2.5% of GDP in Q2 2025, largely due to the rebound in domestic demand and stronger import growth. Crucially, the widening is driven by economic expansion rather than weakening exports, indicating healthier underlying economic conditions compared to previous years.

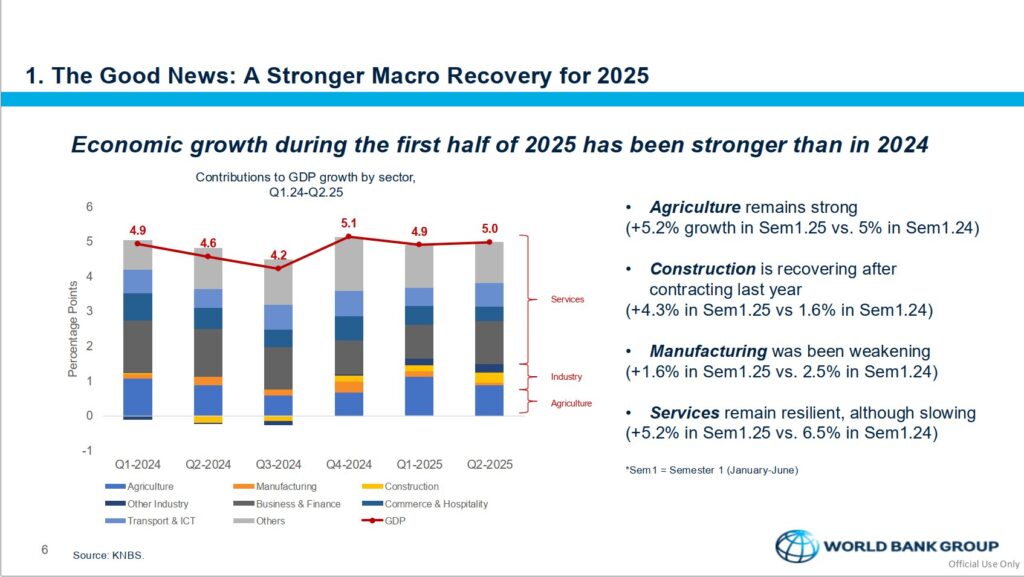

GDP growth in the first half of 2025 outperformed 2024, with strong contributions from agriculture—which expanded above 5%—a resilient services sector, and a notable revival in construction. The rebound in construction, in particular, signals renewed public and private investment, marking a clear turnaround from last year’s contraction and improving prospects for infrastructure-led growth.

Overall, Kenya’s economy is demonstrating firmer stability, supported by improved credit flow, controlled inflation, strong external buffers, and broad-based growth across key sectors. While fiscal challenges and global uncertainties remain, the improving macroeconomic indicators reinforce Kenya’s resilience and provide a solid foundation for sustained recovery and long-term development.

{kind=link}